Dear all,

Many in the financial industry argue that the numbers are all-important. When discussing mainstream finance, decisions are consistently guided by the numbers, which reflect the expected risks and returns.

This involves data, definitions and established procedures that dictate how to calculate value and expectations. With this perspective, it's only logical that sustainable investing has evolved into a data-driven industry.

But what if the most crucial numbers needed are unavailable? What if we lack the conventions and definitions that are customary in 'normal' finance? What if we simply do not have the right data?

I’d say that this leads to erroneous choices, a haphazard approach, overlooking vital elements, and relying on backward-looking investment styles. If we don’t have better data, we simply must have more common sense.

This newsletter has become quite long. Next time I try to keep it shorter (no promises!). At the end you find some of the news from the last weeks.

What is the data we look for?

Imagine you reckon the world needs a bit of sprucing up, and you fancy harnessing the might of money to make that happen. Splendid notion! You might seek out top-notch ideas, companies, and investment prospects that, through their innovations, practices, or processes, edge us closer to this noble aspiration. It's reasonable, isn't it? Yet, sustainable finance doesn't quite operate along these lines.

It's not about ideas or intentions; it's all about DATA! Data serves as a stand-in for ideas and intentions, or so they claim. If your investment goal is risk-return, using data is crystal clear. However, when it comes to sustainability, you definitely need more.

Having been in sustainable finance for some time now, I've encountered a fair amount of data concerning sustainability and the various approaches one can adopt. It's no longer just about using data to enable investing for a better world; it's about risk management, compliance, reporting, and occasionally an endeavour to channel capital towards a sustainable purpose.

Here's a brief overview of ESG approaches from George Serafeim, but there are also other methodologies. In general, finding the right data isn't exactly a walk in the park. With numerous providers, varied definitions, data gaps, and ever-evolving regulations, it often rather feels like aiming at a moving target.

In my view, the myriad types of data and their utilisation in Sustainable Finance can be categorised as follows:

ESG Risk Data: This encompasses information on a business's exposure to Environmental, Social, and Governance risks. Its purpose extends to either excluding or monitoring risks. Examples include the Corporate Sustainability Reporting Directive (CSRD) and the monitoring of climate risks by banks.

ESG Data for Selection: Although sometimes identical to risk data, its application diverges. Rather than integrating ESG risks, this data is employed for selection purposes. This could involve opting for only the top performers on ESG factors or excluding the worst performers. Another approach is to identify those with the best "ESG momentum", such as companies showing the most improvement in ESG scores.

ESG Data for Reporting: Not all ESG factors that are used for selection or risks are typically used for reporting and vice versa. European regulations, particularly those concerning climate (risk) data, necessitate a more comprehensive approach. This includes data on the carbon footprints of investments and scenarios regarding the Paris alignment of portfolios.

Impact Data: This pertains to data concerning the impact of products and services, often quantified in terms of contributions to the Sustainable Development Goals.

Frequently, these approaches or requirements tend to be muddled. While one might champion a best-in-class oil company (ignoring the risk of it becoming a stranded asset), crafting an ESG best-in-class fund could involve numerous polluting industries (accompanied, perhaps, by pledges of improvement).

However, the same cannot be said based on impact data. Nevertheless, it's not always evident (depending on the data source) what positive impact these companies truly make. Some argue that every company generates a positive impact by creating jobs (SDG 8) while conveniently overlooking the negative repercussions.

Moreover, there are several issues associated with all these types of data. The lack of uniform definitions (resulting in varying data across providers), frequent reliance on proxies instead of actual data, subjective and inconsistent measurement methods, and occasional absence of data for entire portfolios pose significant challenges.

I won't delve into all these problems here. On a related note, the EU is actively addressing some of these issues surrounding diverse climate data.

There is no better excuse than data

Let's revisit the application of data and the initial concept of sustainable finance, which, as mentioned earlier, aims for a more sustainable world. One would anticipate that using ESG data facilitates the identification of such investments.

However, the reality is, not surprisingly, often quite different. According to Jan Fichtner, Robin Jaspert and Johannes Petry, the majority of listed ESG funds, constituting the lion's share of sustainable finance, channel capital towards almost the same companies as a non-sustainable benchmark. Therefore, ESG data is primarily employed for categories 1 and 4 in the aforementioned list and, to a lesser extent, category 2.

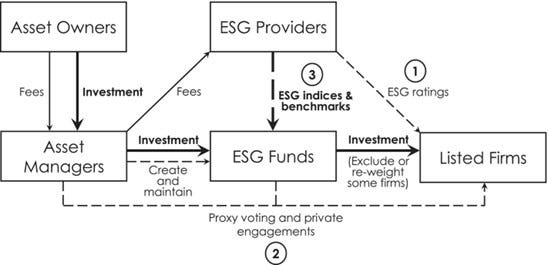

Moreover, they argue that the concentration in the data services industry (ESG providers) results in peculiar effects and interdependencies, exacerbated by the absence of regulation (see figure). Asset owners pay fees to asset managers, who in turn pay fees to ESG providers for the use of their ESG indices/benchmarks or ratings.

ESG providers are responsible for rating companies, while asset managers are tasked with maximizing returns based on the mandate set by asset owners. However, if they must restrict the investment universe (as dictated by data from ESG providers due to the mandate), this limitation might negatively impact performance. Consequently, both asset owners and asset managers have a more or less vested interest in maintaining some ambiguity about what the data truly indicates.

Source: Fichtner et al (2023)

However, given their sustainable mandate, they are obliged to demonstrate some form of commitment. Here’s a few convenient excuses that you often hear:

Yes, we aspire to do more, but the data quality is lacking.

It would be immensely beneficial if we could gauge more about impact, about the actual sustainable practices of organisations. Unfortunately, the quality of such data is even more deficient.

We focus solely on (financial) material ESG data. This isn't an ethical stance but an economic one.

Indeed, all valid points, when viewed from a traditional market perspective.

What does the actual data tell?

A nice paper by Sakis Kotsantonis and George Sarafeim tells the actual data story. Their most important conclusions:

The diversity and inconsistency in how companies report data, especially employee health and safety metrics (more than 20 methods), result in significant discrepancies within the same group of companies.

'Benchmarking,' crucial for determining a company's performance ranking, faces challenges due to the lack of transparency among data providers regarding peer group components and observed ranges for ESG metrics, creating market-wide inconsistencies.

Disagreements among ESG data providers, stemming from varied imputation methods addressing extensive 'data gaps,' lead to substantial discrepancies in reported data.

Interestingly, the disputes among ESG data providers not only exist but intensify with the abundance of publicly available information. This highlights the urgent need for a comprehensive understanding of different ESG metrics and their optimal institutionalization for evaluating corporate performance.

There is much more to it. In addition to ESG data, there is also impact data. This data measures the impact of product and services on society, typically expressed in the contribution to (objectives) of the Sustainable Development Goals (SDGs).

This implies often (but not always!) that for instance solar panels or wind turbine manufacturers get a high score, as well as pharmaceutical companies. Typically, the fossil fuel industry has a low score. These data have the same problems as ESG data: no uniform definition, measurement problems, and inconsistencies.

And this is only in the area where we have the best data available: listed companies. Part of the problems will be overcome in the coming years by standard-setting (such as PCAF for carbon), regulation (CSRD for example). But then, we have large parts of banking activities where data is hard to get: SME bank finance, private debt and equity, venture capital, et cetera.

And since there is no data available, anyone can claim almost everything.

Why better ESG data is not the answer

This last sentence is important. While incorrect or incomplete data give a false sense of knowing what you are doing, no data might also not be the solution. How to proceed?

It has been argued for a long time that “What gets measured gets managed — even when it’s pointless to measure and manage it, and even if it harms the purpose of the organisation to do so”.

While we scrutinize and steer based on data, achieving some predefined targets often misses the mark. I contend that solely focusing on enhancing existing ESG or impact data practices is not the solution, for three reasons.

Firstly, we typically fail to establish boundaries or thresholds, thus allowing compensation for bad behaviour. Average ESG or impact scores offer an incomplete narrative, as it's possible to offset poor ecological performance with commendable social or governance practices. Even worse, we may tolerate ESG risks deemed not 'financially material' – a term from financial sector parlance denoting issues that may not harm financial performance but are inherently undesirable (e.g., harming the environment or people or lacking proper governance).

We can only derive meaningful insights into its sustainability impact by evaluating distinct elements separately from an inside-out perspective (assessing the investment's impact on the external world). (For the experts: yes, this embodies double materiality, but when investing for a better world, focusing on inside-out criteria should be the primary selection criterion.)

Secondly, all data is retrospective, focusing on past ESG or impact performance. It's akin to investing in a company solely based on historical results – a practice no investor would endorse. Analysts typically extrapolate future return potential based on past performance. Why is this not the norm with sustainability data? It makes little sense to predict future contributions to a better world solely based on past information.

Thirdly, and interconnected, most ESG data merely outlines relative performance compared to a benchmark. Essentially, this doesn't assert that a company is doing well but rather, most of the time (especially regarding ecological aspects), doing less harm than the average.

Doing less harm, however, falls short of doing good. Impact data tell a slightly different story, illustrating the contribution of products and services to (achieving) a better world. For example, electric vehicles, solar panels, and wind turbines represent solutions in the energy transition. However, this does not tell anything about the contribution to a future state of the world.

We need better data to save the world

If we aim to use data to safeguard the world, we require new data – data that guides us towards where we need to be, not where we've been. We need data that informs investors about where they can maximise the impact of their money. How do we achieve this? I believe, akin to 'conventional' investing, a structured approach is necessary:

Define a Vision: Establish a vision for the more sustainable world required. Call it a vision or, to align with standard finance, a sector vision or forecast.

Impact Forecasting: Based on this vision, predict the expected impact of an investment. Let's term this a Discounted Impact Flow Model – determining the discounted value of the impact anticipated from the investment.

Identify Leverage Points: Assess leverage points in a transition – understand how investments can be structured to accelerate impact. Incorporate this into the Discounted Impact Flow Model to yield more positive results.

Traditional Calculations with a Twist: Undertake conventional calculations and modelling but be bold enough to base them on parameters reflecting a different world.

Then, invest. Not in ESG, but in future impact. Undoubtedly, this is challenging. But if we lack the right data to save the world, we should trust our values and instincts more than rely on inadequate data.

Other news, apart from many reports in the run-up to COP28:

State of the Climate Action 2023 report: Only one of the 42 indicators of sectoral climate action assessed—the share of electric vehicles in passenger car sales—is on track to meet its 2030 target.

Article about eco-anxiety and reproduction: The impact of climate change on reproductive decision-making is becoming a significant issue, with anecdotal evidence indicating a growing number of people factoring their concerns about climate change into their childbearing plans

How Big oil can derail a transition (links here): social media campaign to boost image among you people, suing Greenpeace and new technologies to protect pumping up.

Degrowth and post-growth thinking is getting traction in the European Parliament, according to this study.

The 2023 Global Report of the Lancet Countdown: One of the best reports, that combines facts on detrimental effects of climate change, root causes and solutions.

Oxfam Novib's report Climate Equality: A planet for the 99%: Understanding the role of the super-rich and affluent individuals (the top 1% and 10% by income) in climate breakdown is crucial for successfully stabilising our planet and ensuring a good life for all of humanity.

And lastly, the Broken record report of UNEP finds that the world is heading for a temperature rise far above the Paris Climate Agreement goals unless countries deliver more than they have promised.

Nevertheless, have a good week!

Take care,

Hans

"Imagine you reckon the world needs a bit of sprucing up, and you fancy harnessing the might of money to make that happen."

What kind of money will you choose to use?

There are six kinds to choose from.

Private Money aggregated through Family & Friends for the purpose of caring for the family and its friends, deployed as patronage for IMPACT, accountable to peer pressure from the family and its friends (with some sensitivity to social shaming from society more generally);

Civic Money aggregated through Church & Philanthropy for the purpose of caring for others, deployed as grants for MISSION, accountable to doctrine or the instructions in the constituting documents;

Public Money aggregated through Taxing & Spending for the purposes of public health, public safety and the public good, deployed as subsidies for POLICY, accountable to constitutional constraints adjudicated in the court, electoral politics and protest in the public square;

Working Money aggregated through Banking & Lending for the purposes of safekeeping, record keeping, and secure transacting (receipts and disbursements), deployed through loans at interest against PROPERTY, accountable to public trust and the principles of safe and sound banking;

Mad Money aggregated through Exchanges & Funds for the purpose of opportunistically and idiosyncratically putting money to work making more money, deployed to finance PROGRESS through speculation on volatility and growth in market clearing prices for securitized shares of large scale financing agreements in the markets for maintaining market clearing prices on such shares, accountable to liquidity in the markets, and transparency for fairness in trading; and

Fiduciary Money aggregated through Pensions & Endowments for the purpose of programmatically providing certainty against certain of life’s future financial uncertainties, deployed through negotiation for SECURITY as the fiduciary purpose of this fiduciary money, accountable under the law of fiduciary duty to the common sense of reasonable people of relevant knowledge and experience for prudence in the exercise of plenary powers of discretionary authority over the deployment of fiduciary money in undivided loyalty to fiduciary purpose.

Your best choice is Fiduciary Money.

But how do we mobilize this money? It it currently trapped in the Markets, trading like mad. Not really useful for sprucing up the world. Only good for keeping Business As Usual delivering more of the same.

We need to set it free.

How do we do that?