#32 The European dream differs from the American dream

Competitiveness is not everything

Hi all,

It's almost Christmas break. And I finally had the chance to look into the Draghi Report on the competitiveness of the European economy. I had time because I took some days off, wanted to do more sports, fell on my gravel bike, and now have to rest. Life is never what you expect, whether it be small or big.

Mario Draghi's report is a must-read (or unavoidable reference) in every serious economic conversation about the European economy. This report is the new Brussels bible, the codeword to get access to a serious policy discussion about competitiveness in the European economy and the go-to analysis for everyone that wants to have arguments for (1) the lagging European economy, (2) reform of finance in Europe, and (3) also an investment plan for Europe.

I have reviewed the report and examined the fundamental, underlying economic assumptions. Is the diagnosis correct? Can this be a successful strategy for radical, sustainable change?

The problem that I have with the report starts in the first sentence:

Europe has been worrying about slowing growth since the start of this century. Various strategies to raise growth rates have come and gone, but the trend has remained unchanged.

Source: The future of European Competitiveness, 2024

Later followed by:

Across different metrics, a wide gap in GDP has opened up between the EU and the US, driven mainly by a more pronounced slowdown in productivity growth in Europe. Europe’s households have paid the price in foregone living standards. On a per capita basis, real disposable income has grown almost twice as much in the US as in the EU since 2000

Source: The future of European Competitiveness, 2024

The underlying assumption is that because the European economy is growing less than the US economy, we are compromising the well-being of current and future generations—the solution: innovation, lower energy prices, and higher productivity. Look at the US!

To start with, I think this is too short-sighted. Yes, total economic activity in the US is growing faster than in Europe. Still, as I explain in more detail below, it is not for the benefit of the ‘bottom’ 90% of the population: while GDP in the US outgrows that of Europe with 47%, the lowest 90% (and especially the bottom 50%) has gained more in Europe (see figure below).

Second, the productivity gains (and the differential with Europe) can only be attributed to one sector: technology. Both hardware and software can explain almost the total differential in value-added developments between the US and Europe (see figures and explanation below). As in the Draghi report:

Excluding the main ICT sectors (the manufacturing of computers and electronics and information and communication activities) from the analysis, EU productivity has been broadly at par with the US in the period 2000-2019 (page 23)

Third, not highlighted in the Draghi report, the US economic model has led to increased public poverty and increased private wealth: while this is a global trend, it is higher in the US than in Europe.

This statistical fact should not be judged in isolation. Economic growth and productivity have risen more in the US than in Europe, but the benefits have reached a small fraction of the population, mainly related to tech sectors. This could happen because of too much market power for a few firms.

The interesting question is: Should we replicate the US's economic “success” or look differently?

My answer is obvious: we should not do that.

Of course, that is not precisely what Draghi proposes, but it remains vague about how we can combine European-style inclusive societies with competitiveness.

Of course, I agree with the three fading external conditions that supported well-being (and overconsumption) in Europe: cheap energy, globalisation, and the end of the Cold War (and the protection of the US).

But I don’t agree with all the answers given.

Replicating the U.S. model—a tech-centric, high-growth paradigm—risks undermining Europe's unique assets. Mariana Mazzucato's insights into mission-oriented public policies suggest an alternative: a shift toward coordinated, goal-driven strategies prioritising societal and environmental well-being over growth for its own sake. Europe's mission should anchor itself in these strengths, leveraging its robust social systems, strong environmental record, and commitment to equity.

The reports commendably frame decarbonization as a dual imperative—necessary for planetary health and economic renewal. However, they acknowledge a critical risk: Without coordination, Europe's climate goals could conflict with its competitiveness. High energy costs, fragmented national policies, and reliance on external suppliers exacerbate this tension.

What is missing is that we could also reduce energy demand. A sufficiency-oriented approach could address this. Rather than emphasizing infinite growth through clean tech exports, Europe could focus on reducing material consumption and fostering local, circular economies. Scaling renewable energy and decentralizing production—akin to Denmark's wind energy model—could further align competitiveness with sustainability.

The reports underscore Europe's innovation deficit, citing regulatory and financial barriers that stifle scaling. However, their proposals—primarily aimed at competing globally in AI and other emerging sectors—risk perpetuating extractive growth models.

Instead, innovation policies should focus on creating regenerative systems. For instance, public investments in renewable infrastructure, eco-industrial parks, and low-carbon housing could be structured around Mazzucato's principles, ensuring state-supported projects serve long-term societal goals.

My combination for the future of Europe would be:

Invest heavily in resource and energy efficiency. This helps to reduce geopolitical vulnerabilities and creates a global niche in terms of competitiveness where Europe already has an advantage (resource efficiency in Europe is already high).

Create more European synergies but remain competitive: We don’t need European, large companies. We need efficient competition and creative destruction that helps innovation.

Yes, we need a better functioning European capital market and better coordination. But we must balance this with diversity (in the financial sector, in ownership structures of companies, etc.) and strict regulations on sustainability to reach resource efficiency.

We need policies that help reduce overconsumption and unnecessary production. This requires mental shifts and more circular economy principles.

We need more public investments in education, innovation, and ‘mission-aligned’ industrial policies. And yes, sometimes, that requires partly rebuilding public capabilities.

That ‘mission-aligned’ industrial policies should concentrate on (1) the areas where Europe need to reduce its strategic disadvantage (energy, resources, point 1), combined with provisioning of forward-looking societal needs (e.g., excellent public transport, health care, culture), and combined with traditional strengths (agriculture, some services sectors, logistics).

There is so much more to say and to do, but not now. Below are some details on the points above, where I delve into the report with a post-growth and degrowth lens. If these proposals sound too radical to you, look at the 71 proposals from the IPBES nexus assessment published this week: many proposals are post- or degrowth alike.

Europe deserves so much better than a comparison with the US. Not all is good in Europe. And yes, we should innovate, improve, and invest. But do not forget: For 90% of the population, Europe has been a better continent than the US in the last 35 years. The European dream is so much richer than the American dream…

Disentangling growth

If you start with the overall growth picture, then, indeed, Europe has done remarkably worse than the US (figure, panel a): a gap of 47% in real terms from 1990 to 2023.1 This figure is relevant to the government's tax income, profits for companies, and the size of the economy. However, taking the increase in persons out (not necessarily working persons!), the difference has shrunk to 9% (panel (b).2 So, you could still say that the US economy performs better per person. GDP growth helps the average American more than the average European.

However, it is never about averages. That is why, in panels (c) to (e), I took out the top of the income distribution for all the years. In panel (c), the top 1% is excluded, which diminishes the frontrunning position of the US to 3%. This implies that the top 1% gained 6% of national income from 1990-2023. We do the same in panel (d) for the bottom 90%. This leads to the opposite conclusion of Draghi: in terms of national income, 90% of the persons were 5% better off living in Europe than in the US from 1990-2023. This difference is even larger if we take the ‘bottom’ 50% (panel (e)): 50% with the lowest incomes gained almost a fifth more (real) income in Europe compared to the US.

The figure below summarises all this: while the size of the economy undoubtedly grew much faster in the US than in Europe, 90% of the population, especially the lower half, was better off in Europe.

If we go back to the Draghi report, is GDP the right indicator for well-being? Not! Is it a good indicator of competitiveness? I would say that depends on where growth comes from. The most significant difference between the US and Europe comes from labour supply. We are ageing as Europe. But we don’t want to have more people entering Europe. Also, in the Draghi report, that seems more or less a given (while I think it would be worthwhile thinking better about it, not only for economic but also for humanitarian reasons). So let’s forget that.

There is only one thing left: productivity growth. Also, there are more behind-the-scenes gross numbers.

Disentangling Productivity growth

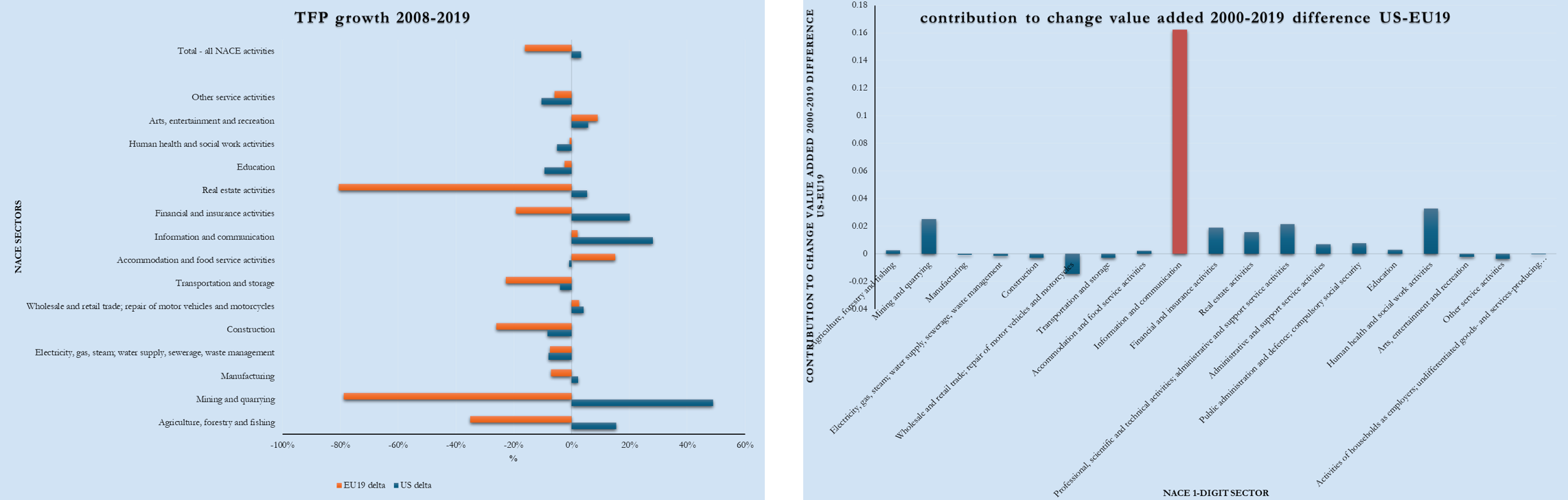

Let’s keep this a little shorter. Of course, there is a lot of nuance to it, but the simple story is: yes, US productivity has increased much more than that of Europe, especially since the turn of the century (see below). For the nerds: this is total factor productivity (TFP) from The Conference Board. It is a difference of 16% points.

However, this is not the entire story. I looked into this database’s productivity growth accounting statistics. This gives numerous ways to see the evolution of value added per sector. Let’s start with the idea closest to TFP's evolution of the economy. Unfortunately, this is a time series only over a shorter period (2008-2019).3 We get from this that (overall) TFP growth in Europe has declined, while it increased (slightly) in the US. Looking at sectors, we see some large discrepancies (especially in real estate, mining, and agriculture). However, this does not tell the whole story because increases in value-added and the share of the sector must weigh productivity.

To keep it simple, I took value added by sector, its contribution to (overall) value added, and then the difference between the US and Europe from 2000-2019. The story is then quite straightforward. The sector that is responsible for the largest difference between the US and Europe is Information and communication. On a more disaggregated level, the top 5 that makes the difference is:

J62-J63 Computer programming, consultancy, and information service activities C26 Manufacture of computer, electronic and optical products

J58-J60 Publishing, motion picture, video, television programme production; sound recording, programming and broadcasting activities

Q86 Human health activities

C26-C27 Computer, electronic, optical products; electrical equipment

In other words, it is foremost tech and related (social) media activities (except the ‘value added’ (or costs) generated by health care). This is also what Draghi concluded. However, the recommendations are more or less to replicate the US story.

It is important to note that we can not separate GDP development (and its distribution) from productivity increases in this case. For instance, we know that the increase in billionaires in the US is heavily connected to the same sectors where we see the most significant productivity gains.

A sufficiency and post-growth lens to competitiveness

While reading the Draghi report, I wondered if it would lead only to incremental changes or to more radical change. Integrating a post-growth and sufficiency perspective into the analysis offers an alternative to both degrowth and growth-centric paradigms. I have found eight points on which post- or degrowth ideas differ from the analysis of the Draghi report.

1. Emphasis on Resource Efficiency and Circular Economies

Current Report Focus: Advocates for resource efficiency and technological innovations to maintain competitiveness.

Degrowth & Sufficiency Angle: While resource efficiency aligns with ecological goals, it risks reinforcing a "rebound effect" where efficiency leads to increased consumption. Sufficiency promotes limiting resource use to absolute necessities, moving away from the idea that efficiency can sustain indefinite growth.

Post-Growth View: Encourages systemic redesign of economies toward circularity and long-term resilience. This would involve embedding repairability, sharing economies, and extending product life cycles rather than focusing solely on efficiency metrics.

2. Focus on Competitiveness

Current Report Focus: Prioritises global competitiveness by reducing energy costs and leveraging advanced technologies.

Degrowth & Sufficiency Angle: Competitiveness often drives overproduction and overconsumption, which degrowth and sufficiency frameworks oppose. Instead, emphasis should shift to well-being, equity, and ecological balance. Competitiveness is not a goal in itself.

Post-Growth View: Supports fostering local and regional economies that prioritise cooperative trade and mutual benefit rather than cutthroat competition. Competitiveness should serve the well-being of people and ecosystems.

3. Renewable Energy Transition

Current Report Focus: Expands renewable energy to decarbonise and reduce import dependency.

Degrowth & Sufficiency Angle: Degrowth warns against industrial-scale exploitation of renewables, which may require mining rare materials and disrupt ecosystems. Sufficiency suggests prioritising smaller, community-based projects and energy reductions to avoid excess demand.

Post-Growth View: Advocates for renewable transitions that emphasise equity, decentralisation, and resilience. For example, renewable projects should focus on local ownership and integration with energy conservation measures.

4. Technological Innovations

Current Report Focus: Proposes reliance on AI, hydrogen, and advanced digitalisation to optimise energy use.

Degrowth & Sufficiency Angle: Be cautious when viewing technology as a panacea. Many innovations are resource-intensive and fail to address the root causes of unsustainability. Sufficiency prioritises low-tech, less resource-dependent solutions.

Post-Growth View: Technological advancements should focus on regenerative practices and low-impact designs. Innovations must serve human and ecological well-being rather than growth for its own sake.

5. Economic Decentralisation

Current Report Focus: Highlights citizen engagement and decentralised solar as emerging solutions.

Degrowth & Sufficiency Angle: This angle is strongly aligned. Decentralisation supports community empowerment, reduced dependency on global supply chains, and localised sufficiency.

Post-Growth View: Enhances decentralisation by promoting cooperative energy models, community decision-making, and inclusive governance structures.

6. Market-Based Solutions

Current Report Focus: There is heavy reliance on carbon pricing, Power Purchase Agreements (PPAs), and market mechanisms to drive renewable adoption.

Degrowth & Sufficiency Angle: Criticises market solutions for prioritising economic incentives over equitable access. Sufficiency frameworks advocate for public investment in commons-based energy systems rather than market-led initiatives.

Post-Growth View: This view supports blended systems where public ownership, cooperative models, and market tools coexist, prioritising affordability and ecological regeneration over profit.

7. Social Equity and Inclusion

Current Report Focus: Acknowledges risks to vulnerable households and SMEs during transitions but maintains a growth-centric framing.

Degrowth & Sufficiency Angle: Proposes prioritising equity and universal access to basic needs. Energy transitions must address systemic inequalities and prevent rising energy poverty.

Post-Growth View: This view focuses on designing inclusive systems where economic activity enhances social well-being. Policies could include universal basic energy access, subsidies for sustainable housing, and retraining programs for green jobs.

8. Critique of Industrial Policies

Current Report Focus: Sustains energy-intensive industries through innovation and competitive pricing.

Degrowth & Sufficiency Angle: Opposes policies that uphold industries with high ecological footprints—advocates for reducing industrial output to sustainable levels while focusing on sufficiency in production and consumption.

Post-Growth View: Encourages shifting industrial focus to regenerative and circular models, where industries contribute to ecological restoration and local community resilience.

Based on this analysis, some ideas to improve the future of Europe:

Shift Focus from Growth to Well-Being:

Replace GDP-based success metrics with social and ecological well-being measures, such as the Genuine Progress Indicator (GPI).

Promote Sufficiency in Energy Use:

Adopt energy reduction targets alongside renewable energy expansion to ensure sufficiency rather than excess production.

Localise Economies:

Build self-sufficient regional economies to reduce dependencies on global trade, focusing on localised energy, food, and material systems.

Redesign Economic Systems:

Integrate circular economy principles that minimise waste, promote sharing economies, and encourage product longevity.

Equitable Transitions:

Establish mechanisms, such as subsidies, retraining, and participatory decision-making processes, to ensure that vulnerable groups and SMEs are supported during energy and economic transitions.

Move Beyond Technological Optimism:

Balance the role of high-tech solutions with low-tech, scalable, and community-driven alternatives that align with ecological limits.

Foster Community Ownership:

Encourage cooperative ownership of renewable energy projects and infrastructure to ensure inclusive and democratic participation.

Systemic Support for Low-Impact Lifestyles:

Incentivise behavioural shifts towards sufficiency, such as reduced work hours, public transport usage, and low-consumption living.

There is so much more to say, write, and add. But I will stop here—next time.

Have a lovely Christmas (and I will start sporting again in the coming weeks),

Hans

There are different ways to calculate GDP growth. In this case, I took GDP constant prices (not ppp corrected) and used the data from WID.world. If you use IMF data, the difference is 50%.

Technically, from here, I took National Income. Slightly other definitions and results are the same.

I used the TFP index, contributions to value-added growth per person employed.