#25 Let’s heat the debate but keep our heads cool

About climate finance.

Hi all,

It was a refreshing summer for me, at least. I tried to concentrate on some more extended writing and swimming - a perfect combination, but I don’t know what was the most refreshing part. Some of the writings will be public later, and for the swimming, I don’t think most of you care. At least I enjoyed it.

Now that everything has started again, I want to pick my newsletter. And I must be honest: it will not be as frequent as I would like. But that’s life: it is never as perfect as you would wish (but on the other hand, if it reaches the perfectionism that you have imagined, you’ll probably find out that it is also not perfect…and you’ll strive for something even more perfect, and then…well, you know).

My mentally refreshing summer was in the midst of a record-breaking summer. We are becoming desensitized to this kind of news; for the past 13 months, each month has set a new record for global temperature. There’s a fair chance that we will exceed the 1.5C threshold outlined in the Paris Agreement by the early 2030s. We should all feel the urgency of a warming planet to expedite the energy transition. However, heat stress appears to be leading to inaction.

I will discuss climate finance in this newsletter. Despite the growing crisis, we still need to mobilize the necessary capital to achieve the energy transition. And there is a lot to do: fighting climate finance distractions, understanding how we can mobilise capital in the right direction and, more importantly, stopping financing what should be phased out.

We need to heat the debate but keep our heads cool.

Enjoy

Distraction

I notice a shift in the conversation. Call it a distraction. Instead of discussing divestments from fossils, climate pledges and all other complex stuff (that hurts business), we have two considerable ways in finance to say that you do a lot on climate finance or expand your business. In the run-up to COP29 not a good sign (and some are already predicting that it will be a failure). The two strategies that I see are transition finance and sustainable (or climate) finance innovation:

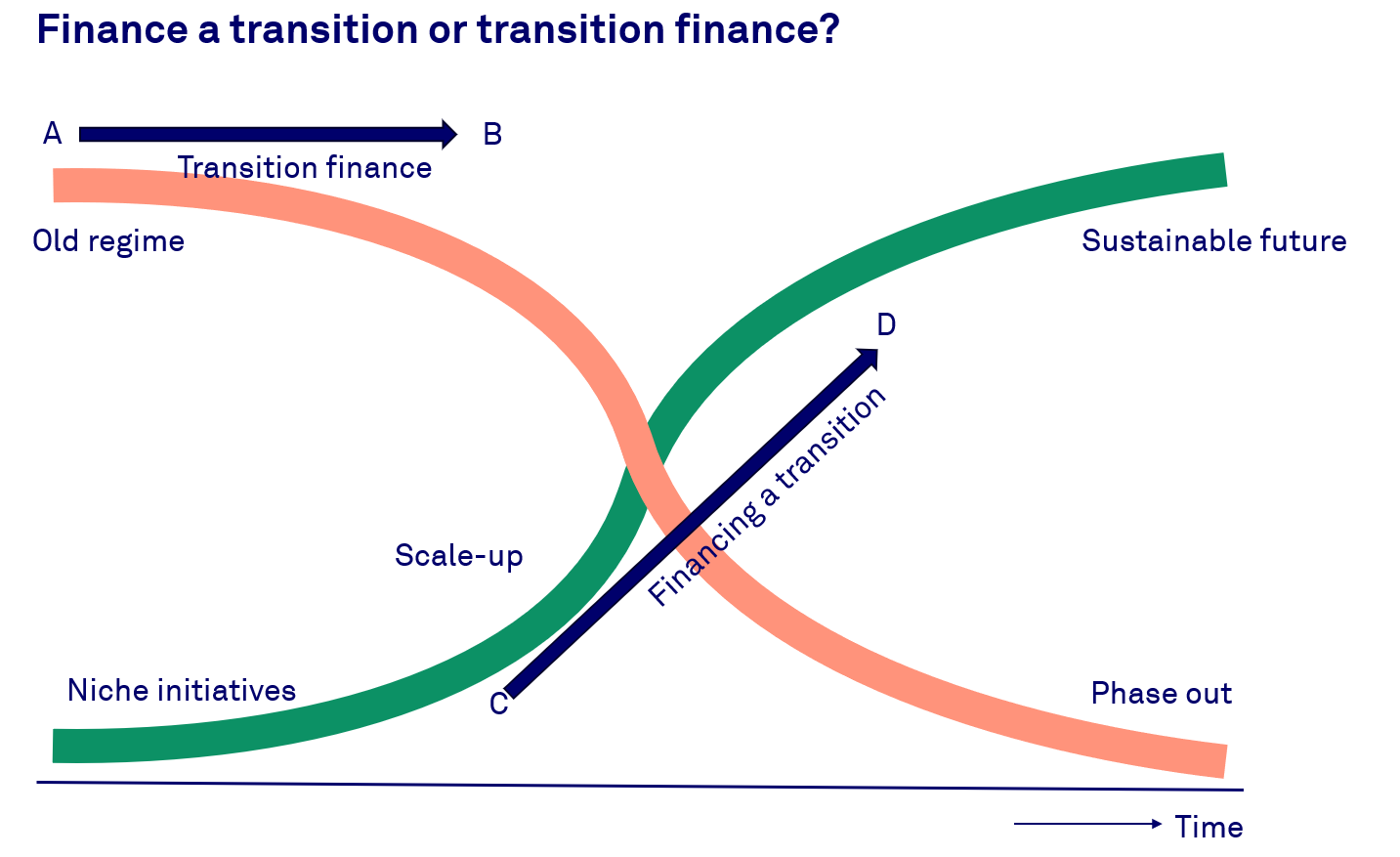

Transition finance: In mainstream terms, this is everything that smells less brown at a company level. I tried to show it in a so-called transition curve (see below). If a high-emitting company goes from A to B, it is called ‘a transition’. However, it is not near the goal that should be reached. Client Earth has an excellent paper about Transition-Washing. Transition-washing occurs when transition finance is provided to entities that are not, in fact, or have no meaningful intention to transition their business to net zero greenhouse gases at the pace required to achieve the Paris Agreement temperature goals.

This transition finance is different from financing a transition. You start scaling a societal transition by funding companies or projects contributing to that transition (from C to D). And I mean genuinely contributing with clear ideas on becoming entirely sustainable. This can sometimes go from highly polluting to sustainable, but there are few transitions where the winners of the old regime were also the champions of the new one. So, for a large part, it is a distraction.

Innovative climate finance: Climate finance encompasses various financial instruments to address climate challenges. These include grants and loans from public institutions like governments and multilateral funds, green bonds, carbon taxes, and private investments. All these financial resources are directed either toward mitigating the impacts of climate change or enhancing resilience and adaptation to the new realities we face. This seems good. However, there are two problems with it: it is, in general, very, very small, and you can question if it, in the end, helps the transition enough. Below, you’ll find my more elaborate analysis of this.

So, if financial instruments and a new term (transition finance) do not work, how can we progress? The answer is (as always) a more fundamental shift. We have to look at the structure of the financial system to make it work in favour of an energy transition.

This article on the World Resources Institute website already gives some clues. A quote:

There’s no formal governance relationship between climate finance and the global financial system. But climate finance, whose principal objective is to address the impacts of climate change, must use the global financial system, which facilitates the flow of climate finance and allocates resources for climate-related activities. Whether it’s a loan made by a development bank to build a solar farm, or a hurricane-battered country seeking payment for damages through sovereign insurance, these “vehicles” travel through the global financial system.

The trend in the last few years was that supervisory authorities (championed by the ECB) have done much on climate risks. The better risks (physical and transition risks) are recognized, the more capital would be directed towards the energy transition, is the idea. But that is probably not enough; mitigating risks differs from contributing to a solution. What many of us know in sustainable finance is that if you want to build a low-carbon equity portfolio or a low-carbon business banking portfolio, you’ll be more likely to end up with sector biases to services and tech and not a bias towards climate tech or a protein-transition portfolio or circular economy.

So, more is needed. Many look at financial institutional governance, with post-war representatives still at the International Monetary Fund and World Bank.

For example, the Bridgetown initiative, which makes good points:

Stronger Representation: Increase the voice of developing countries in global financial institutions.

Debt Sustainability: Reform the IMF and World Bank's Debt Sustainability Assessment to include climate investments.

Credit Rating Overhaul: Revise credit rating methodologies to address biases against vulnerable countries.

Concessional Financing: Expand eligibility beyond GDP per capita to include climate vulnerability.

Global Carbon Pricing: Develop a just global carbon pricing framework.

Liquidity Support: Enhance access to early intervention liquidity and extend IMF financing options.

Debt Resilience: Incorporate natural disaster clauses in all debt instruments by COP29.

Increased Financing: Mobilize $1.8 trillion annually for climate action and SDGs, with significant private sector involvement.

Innovative Funding: Establish new financing sources, including levies on fossil fuel profits, and fully capitalize the Loss and Damage Fund.

I think this will not be agreed upon in Baku…

Ultimately, it is probably more about transforming the financial sector to mobilise capital to finance the energy transition.

Funding gaps

(based on this article, in Spanish)

Many view climate finance as a critical bottleneck in accelerating the energy transition. Climate finance encompasses a broad range of financial instruments to address climate challenges. These include grants and loans from public institutions like governments and multilateral funds, green bonds, carbon taxes, and private investments. All these financial resources are directed either toward mitigating the impacts of climate change or enhancing resilience and adaptation to the new realities we face.

Current financial flows need to increase at least threefold to meet the Paris Agreement targets. Despite significant efforts, there remains a substantial shortfall in the necessary funding.

This issue is often described as a 'funding gap'—a mismatch between the projects that require financing and the capital available to support them. The Climate Policy Initiative estimates that USD 6.2 trillion in climate finance is needed annually between now and 2030, increasing to USD 7.3 trillion by 2050, to achieve Net Zero—nearly USD 200 trillion.

But does this mean we need to make that much extra capital available for the energy transition? The reality is more complex.

Governments and the financial sector continue to channel substantial funds into fossil energy. According to the International Monetary Fund, global fossil fuel subsidies amounted to USD 7 trillion in 2022, or 7.1% of global GDP. This isn't about finding more money but about reallocating existing funds. We must defrost capital from stranded assets and redirect it toward the energy transition.

But there is a reason why capital is still wrongly allocated. The problem lies in the higher returns from fossil fuels compared to renewables. This reflects an "asymmetry of finance": it's easy to profit from exploiting nature, where resources and externalities are underpriced, leading to carbon emissions. The opposite—investing in restoring nature—is more challenging, as it often yields limited financial returns despite creating significant public value. Redirecting capital requires a shift in thinking, recognizing that private gains should not come at the expense of public well-being.

Innovative climate finance

Due to this financial asymmetry, innovative financial mechanisms are emerging to make climate mitigation finance viable. Markets naturally respond to demand by creating supply and vice versa.

The good news is that progress is being made—market volumes are increasing across the board. However, these volumes are still far from what is needed to meet global climate goals.

Firstly, there is a growing shift towards blended finance, where public funds cover initial losses and risks, thereby leveraging private capital. In 2023, blended finance reached a five-year high, with climate-related blended financing increasing by 107%, from USD 5.6 billion in 2022 to USD 11.6 billion in 2023. While this progress is encouraging, these efforts remain limited in the broader context of what is needed to address the climate crisis.

Secondly, the market for green bonds—loans aimed at funding sustainability projects, including climate initiatives—had a strong first quarter in 2024, following a solid performance in 2023. The total issuance is on track to reach USD 1 trillion in 2024. However, the downside is that the largest issuers, primarily governments, have increased their spending on fossil fuel subsidies.

Thirdly, carbon markets represent an even more innovative approach. These markets exist partly because regulators have introduced carbon caps and pricing, the largest being the EU Emission Trading System (ETS). In 2023, approximately 12.5 billion metric tons of carbon permits were traded globally, with the market's value reaching USD 949 billion, a 2% increase from 2022. The ETS accounted for 87% of the total global population. This market is expected to expand further if governments implement stricter emissions regulations.

The current focus is on Voluntary Carbon Markets (VCM), where nature restoration efforts create revenue through the sale of carbon credits. However, these markets are fraught with controversy, including concerns about standards, greenwashing, and project profitability. While VCMs promise innovative solutions, they are still in their early stages, with a projected global volume of just USD 3 billion this year. Given the magnitude of our challenges, this amount is barely a drop in the ocean.

We must keep our heads cool

Climate finance is gaining traction, with innovative solutions drawing even more attention. However, it’s not enough to cool the planet despite the buzz. The additional funding needed for climate mitigation and adaptation won't just come from financial innovations—it will come from solid policies. These should include a global carbon tax, eliminating fossil fuel subsidies, mandatory standards for emerging markets like carbon credits, and a firm commitment from governments to phase out fossil fuels. Such measures would create a level playing field, making it easier for mainstream finance to support the energy transition without relying solely on financial innovation. We must keep our heads cool: financing the energy transition is more helped with less favouring fossil fuel finance than financial innovations.

Thanks for reading,

Be kind

Hans